US stocks notched fresh record highs Tuesday in a session defined by surging semiconductor names, easing oil prices, and a steady stream of market-moving headlines through the trading day.

US stocks notched fresh record highs Tuesday in a session defined by surging semiconductor names, easing oil prices, and a steady stream of market-moving headlines through the trading day.

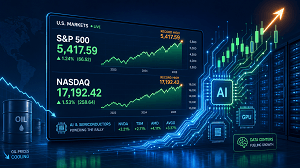

Semis lead as S&P 500, Nasdaq hit records

The S&P 500 and tech-heavy Nasdaq Composite both closed at all-time highs, powered by renewed enthusiasm for the AI trade and a sharp move higher in semiconductor stocks. Chipmakers rallied ahead of AMD’s earnings, with the PHLX Semiconductor Index climbing to new records as investors rotated back into high-growth tech after last week’s geopolitics-driven pullback. The S&P 500 finished up about 0.8%, while the Nasdaq gained just over 1%, underscoring how dominant AI-linked names have become in driving the broader market’s advance.

Oil cools, but Iran war shock still looms

Oil prices eased after Monday’s conflict-driven spike, though both Brent and WTI futures remained well above the $100 mark, reflecting ongoing supply risks from the US‑Iran war. Brent slipped roughly 2%–3% to around the low-$110s, while WTI dropped more than 3% to just below $103 as a fragile ceasefire appeared to hold through Tuesday’s session. Deutsche Bank economists noted that while the US has become far more insulated from foreign oil shocks over the past decade, it is still a net importer of crude and remains exposed to globally set prices. That vulnerability is showing up at the gas pump, where US drivers are facing significantly higher prices as disrupted Middle East flows ripple through refined products markets.

AI boom powers markets — and inflation

Live coverage highlighted how AI has become a twin force in the US economy: a powerful growth driver and a new source of inflation pressure. Bank of America economists pointed to consumer spending and AI-related investment as the main pillars supporting domestic demand, while other components of final demand have mostly softened. Goldman Sachs, meanwhile, flagged that intense build‑out of AI infrastructure — from data centers and chips to power — is already nudging core inflation higher by raising electronics and electricity costs, an effect they expect to continue over the next year.

Chip trade broadens beyond Nvidia

The chip story is no longer just about GPUs. Live updates showed Micron and Intel surging to record intraday highs as investors piled into the broader semiconductor supply chain, from memory and storage to equipment makers. Micron’s stock has exploded higher since late March, helped by booming demand for memory used in AI workloads and a recent credit upgrade that reinforced confidence in its balance sheet. Intel jumped sharply after reports that Apple is exploring using both Intel and Samsung to manufacture core processors in the US, a potential long‑term shift away from its heavy reliance on TSMC. ETF flows are echoing this move: trading volumes in semiconductor and leveraged chip funds have picked up, and indexes tied to memory makers have posted outsized gains over the past year.

SpaceX fuels a race in ETFs — before the IPO

One of the more speculative threads in the live blog was the scramble to gain exposure to SpaceX before its widely anticipated IPO. The Elon Musk‑led company has reportedly filed confidentially with the SEC and is eyeing a potential June listing that could value it around $1.75 trillion and raise tens of billions of dollars. ETF providers are already launching or tweaking space‑themed funds to ensure they can add SpaceX quickly once it goes public, taking advantage of new “fast‑entry” rules that allow some megacap IPOs into major indexes like the Nasdaq 100 in as little as 15 trading days. That speed matters: funds that manage to own SpaceX early could capture outsized demand if the stock trades like other blockbuster tech listings.

SEC floats big shift on earnings reports

On the policy front, traders also watched a notable proposal out of Washington: the SEC is considering allowing US public companies to opt out of the traditional quarterly earnings cycle in favor of semiannual reporting. The move would roll back a decades‑old requirement for companies to file detailed results four times a year and has long had the backing of President Trump, who argues that less frequent reporting could help firms focus on long‑term strategy. Under the proposal, companies and investors could largely decide the interim update cadence that best fits their business needs, though critics worry it might reduce transparency and increase information gaps between retail and institutional investors.

Labor market, bonds, and crypto add cross‑currents

Beyond stocks and oil, the live blog captured a market grappling with mixed macro signals.

- Long‑term Treasury yields again pushed near the 5% “danger zone” on the 30‑year bond, a level that has repeatedly tightened financial conditions and triggered short‑term equity pullbacks in recent years.

- The latest JOLTS data showed job openings essentially flat in March, with hiring picking up from recent lows but layoffs ticking modestly higher.

- Coinbase announced plans to cut hundreds of jobs as part of a restructuring aimed at adapting to both a weaker crypto backdrop and the rise of AI, even as the stock bounced on hopes that cost cuts will support margins.

Taken together, Tuesday’s live coverage painted a market that is learning to live with geopolitical shocks and higher rates, leaning heavily on AI‑driven earnings momentum to keep indexes at record highs while watching bond yields, energy prices, and labor data for signs that the “teflon” rally might finally crack.